When Sarah first considered selling her manufacturing business, hiring a broker felt like the obvious choice. “They handle everything,” she thought. “I can focus on running my business while they find buyers.”

What Sarah didn’t realize was that her decision to use a broker would ultimately cost her more than a luxury home.

The Staggering Math Most Sellers Don't Calculate

Let’s start with the numbers that should make every business owner pause. According to industry data, business brokers typically charge success-based commissions ranging from 7-10% of the sale price. On paper, this might seem reasonable—after all, you only pay if they succeed, right?

But let’s do the math:

- $3 million business sale at 8% = $240,000 in fees

- $5 million business sale at 7% = $350,000 in fees

- $10 million business sale at 8% = $800,000 in fees

To put this in perspective, that $350,000 commission on a $5 million sale could:

- Fund a comfortable retirement for many entrepreneurs

- Purchase a vacation home outright

- Start your next venture with significant capital

- Provide college funding for multiple children

Instead, it’s going directly into your broker’s pocket.

The Hidden Fees Nobody Talks About

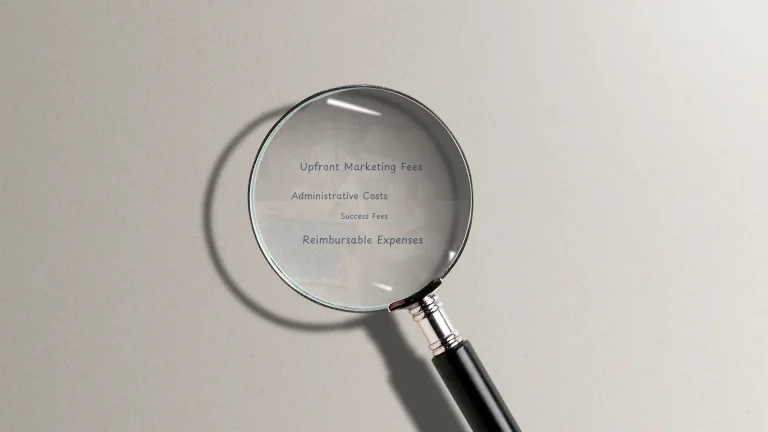

The commission is just the tip of the iceberg. Most brokers also charge additional fees that eat into your proceeds before your business even sells:

Upfront Marketing Fees: Many brokers charge $5,000-$15,000 for “professional marketing packages” and business valuations. These fees are non-refundable, whether your business sells or not.

Administrative Costs: Document preparation, listing fees, and “processing charges” can add thousands more to your total cost.

Success Fees: Some brokers charge additional “success fees” on top of their standard commission, particularly for larger deals.

Reimbursable Expenses: Travel costs, marketing materials, and due diligence expenses that get passed back to you.

When you add these costs together, your total broker expense can easily exceed 10% of your sale price—sometimes reaching 12-15% for smaller businesses.

The Misaligned Incentives Problem

Here’s where the business brokers’ model gets truly problematic: their incentives aren’t always aligned with yours as the seller.

Speed Over Price: Brokers earn their commission when deals close, not when they maximize your sale price. A broker makes nearly the same commission whether your business sells for $4.5 million or $5 million—but that $500,000 difference is enormous to you.

Volume Over Value: Many brokers work on volume, juggling dozens of listings simultaneously. Your life’s work becomes just another deal in their pipeline.

The “Bird in the Hand” Mentality: When the first decent offer comes in, brokers often pressure sellers to accept rather than wait for better terms. Their thinking: “A sure commission today is better than a possible higher commission tomorrow.”

One business owner shared his experience: “My broker kept pushing me to accept an offer that was $800,000 below my target price. He said the market was ‘cooling off’ and I should ‘take what I could get.’ Later, I discovered he had three other deals pending and needed quick closings to meet his quarterly targets.”

The Control Problem: Your Sale, Their Rules

When you hire a broker, you’re essentially handing over control of the most important financial transaction of your life. Brokers decide:

- How your business is marketed and to whom

- Which buyers get access to your confidential information

- How negotiations are conducted and what terms are acceptable

- The timeline and process for due diligence

Many business owners report feeling sidelined during their own sale process. As one entrepreneur put it: “I felt like a spectator at my own game. The broker was making decisions about my company’s future without really consulting me.”

The Success Rate Reality Check

Perhaps most damning of all: the success rates. Industry data shows that only about 10-20% of businesses listed with brokers actually sell. This means roughly 80-90% of business owners who hire brokers end up paying upfront fees for unsuccessful sales attempts.

Even worse, businesses that sit on the market for extended periods often become “stale listings,” making future sales more difficult and potentially reducing the final sale price.

Red Flags: When Brokers Make It Worse

The High-Price Hook: Be wary of brokers who immediately agree to your asking price without proper analysis. This is often a tactic to win your listing, followed later by pressure to reduce the price when no buyers materialize.

Exclusive Agreements: Many brokers demand exclusive listing agreements lasting 6-12 months or longer. If the broker proves ineffective, you’re stuck paying their fee even if you find your own buyer.

Lack of Industry Expertise: General business brokers may not understand the nuances of your specific industry, leading to poor buyer targeting and unrealistic expectations.

Poor Communication: If a broker is difficult to reach or provides infrequent updates, this often indicates you’re not a priority in their portfolio.

Alternative Approaches That Save You Money

Direct Sales: Many successful business sales happen through direct outreach to strategic buyers, industry contacts, or qualified individuals. This approach eliminates broker fees entirely.

Boutique Acquisition Firms: Some specialized firms focus on direct acquisitions, working directly with business owners without traditional broker fees. These firms often have deeper industry expertise and aligned incentives.

Limited Service Options: If you need some professional help but want to maintain control, consider consultants who charge flat fees for specific services rather than percentage-based commissions.

Industry Networks: Professional associations, industry conferences, and peer networks can be excellent sources for finding qualified buyers at no additional cost.

Making the Right Choice for Your Situation

This isn’t to say that brokers are never the right choice. For some business owners—particularly those with limited time, no industry connections, or complex situations—a broker might provide valuable services despite the cost.

However, before signing any broker agreement:

Negotiate Commission Rates: Everything is negotiable. Some experienced sellers have negotiated rates as low as 3-5%, particularly for larger transactions.

Understand All Costs: Get a complete breakdown of fees, expenses, and potential costs before signing any agreement.

Verify Track Record: Ask for specific examples of similar businesses the broker has sold in the past 12-18 months.

Maintain Some Control: Insist on regular communication, approval rights for marketing materials, and input on potential buyers.

The Bottom Line

Your business sale represents the culmination of years—perhaps decades—of hard work, sacrifice, and dedication. The difference between a 7% broker commission and a direct sale can literally be hundreds of thousands of dollars.

Before automatically assuming you need a broker, consider the true cost: not just the commission, but the loss of control, potential misaligned incentives, and opportunity costs of an extended sales process.

Take time to explore your options. You might discover that the “easy button” of hiring a broker is actually the most expensive choice you could make.

What's Your Next Step?

If you’re considering selling your business, start by getting an objective valuation and understanding your options. Many business owners are surprised to learn about alternatives to traditional broker relationships that can save significant money while maintaining control of their sale process.

The goal isn’t just to sell your business—it’s to maximize the value you receive while preserving your legacy and ensuring a smooth transition. Sometimes the best way to achieve that is to keep more of your hard-earned proceeds in your own pocket.

Ready to explore your exit options without the pressure of broker fees? Download our free Exit Readiness Toolkit to learn how successful business owners are maximizing their sale proceeds while maintaining control of their exit process.